This post is for someone who is struggling to get started on becoming financially stable. I’m providing the bare bones to get started despite what your long-term plans may be or specifics on your financial situation.

There’s so much information out there, and very quickly someone can come across advanced concepts that may derail them from even getting started. For example, for someone in debt who would search about repayment, very soon they would come across an article that explains how you could make more money investing than paying off their debts. Even if the math is correct, in this situation, many people don’t end up doing either (I was one of them!).

I strongly suggest that if you are just getting started, focus on consistently saving and paying off debt for 6-12 months. Unless you won the lottery or have an unexpected amount of money piling in your bank account, awareness and stability should be your focus.

The long-term phases for financial freedom are typically:

- Financial Awareness: Obtain clarity on your current situation.

- Financial Stability: Execute a consistent plan for saving and debt reduction.

- Financial Freedom: Investor mindset focused on acquiring and living off of assets.

I will take you through Phase 1 and set you up for Phase 2. What I cannot do is execute consistently for you, that’s what only you can do for yourself.

I’m the first one to fall into analysis paralysis, so I know how hard it is to jump into things especially managing your finances. I am going to ask you to take action while you read this post. Do not read and then plan to do it later, you know you won’t do this later.

We have 5 steps. Here we go…

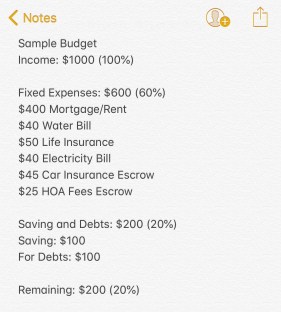

Step 1: Write down your net income and fixed expenses

I wrote this information down on a note in my iPhone, so please do not complicate this. Yes, there are templates and budgeting tools, but if you are just getting started, just write this down right now. I actually like having it on my phone. Although I’m starting to use excel templates, I won’t access them as regularly, so just open up a note on your phone and get started.

Net Income is the money that you take home, what is deposited into your account. This can include child support, rental income, etc. If your income varies from month to month, write down the amount you can count on every month.

Fixed Expenses are those expenses that are consistent and usually the same amount every month. This includes your mortgage or rent, car payment or other loan payments. I like to include my utilities here, too. For utilities I write down an average or a maximum amount to ensure it’s part of my budget. Other monthly fixed expenses could include gym membership or any subscriptions such as iTunes app purchases, Netflix, magazines, etc. Keep these smaller non-necessities at the bottom, but still under fixed expenses (you’ll see why in a sec).

Other items I like to include here are expenses that happen annually or semi-annually, for example, car registration or Home Owners Association fees. What I do is create a sort of escrow account. Let’s say I have to pay $300 annually for HOA, I would add $25 expense for it every month and call it HOA Escrow.

Before we move to step 2, calculate the % of your income that you are spending on fixed expenses. For example, if you are taking home $1000, and the total fixed expenses adds up to $700, divide 700/1000 to get .7 which equals 70%. Write this percentage next to the words “Fixed Expenses” on your document.

This simple calculation should already give you an increased awareness of your financial situation, but let’s continue.

Step 2: Determine Saving and Debt Reduction Goals

Assuming you are just getting started with this and are not consistently saving, we are now going to calculate how much you should be saving and if you have debts, how much additional you should be paying on those. For this exercise, I am going to refer to the 50/30/20 rule. I don’t fully love this breakdown, but the 20% to savings and debt makes sense to me as a starting point. Take your net income and figure out what is 10% of it. To continue my previous example, if you are taking home $1,000, 10% of that would be $100, 20% would be $200.

Write down this amount and percentage below like this:

This is your goal saving and debt reduction amount. How does it feel – do-able? Too much or too little? For most people who are just starting off, this will sound like too much money, so let’s adjust it in Step 3.

Step 3: Lower Your Fixed Expenses and Commit to Saving

Before we get into the most important part of this post on budgeting, how much money do you have left? Calculate the difference and the percentage. In my example above, this is what it would look like:

The typical 50/30/20 model says the 50 percent should be your “needs”, but that’s really hard to track and adds complexity as you are having to categorize your expenses. I prefer to simply break this down by fixed and variable expenses. Logically, the only way to have any flexibility in your life is to get fixed expenses as low as possible, and on an automatic payment system, so you’re not even thinking about it. You really only have to do this once and do it right, and rarely touch this budget unless something changes.

So, if your fixed expenses are about 50% or lower, move on to Step 4. If not, keep reading.

If your fixed expenses were 80% or more, you don’t have anything left. This is a huge problem. If your expenses are above 50%, look at your fixed expenses and decide what you can live without to get as close to 50% as possible. If you had any of the “smaller” subscription expenses, these need to get cancelled today. You can workout at home and any entertainment expenses can go! My husband and I have never had cable. Once we decided we were going to reduce our dining out, we did purchase a TV and an antenna (one-time $30) so he could watch some sport games instead of going out to the bars.

Your strategy on how to reduce your fixed expenses will be completely personalized and depend on your situation. If you are paying a mortgage, keeping your house should be a priority and you should look to reduce other expenses. However if you are renting and your rent takes up more than 30% of your income, you are living above your means. This is also true for a mortgage, but I wouldn’t recommend you sell for this reason if there are other ways to manage your expenses or increase your income. If you are renting, some ideas include getting roommates, living in a different part of the town, or go live with your parents or family members for a discounted rent price.

I have never had a car payment. I bought my last two cars in cash and otherwise used public transportation which I understand is not convenient in every city, but if you want to get your life together, you have to be very frugal and think about your options. A car payment is usually the second biggest expense for people. If you have already signed a contract and it doesn’t fit in your budget, you still have options such as renting your car out on Turo or doing Uber/Lyft to help with your payments. If you are really looking to get out of this, see swap a lease. Also if you do have an old car without a payment, make sure you’re taking care of it. You want this to last as long as possible.

Your goal should be fixed expenses at 50% of your income, so know what amount this is. If you are at 75%, make a goal to get to 65%. What can you eliminate? What can you reduce? What will you do today to help you get there? What can you do once contracts end to reduce this amount?

If your fixed expenses are too high, you will not able to save or reduce your debt which will keep you broke.

How does your breakdown feel so far? Is the initial 20% to saving and debt reduction now do-able? If you don’t have debts, then commit to 20% savings. If you are still really tight, can you do 5% for each or even 2%? You have commit yourself now that is what you want in your life. As a base guide, if your fixed expenses are at about 65% or less, I am going to challenge you to commit to set aside 20% for savings and debt reduction.

It’s important to do this before you look at the rest of your expenses because you will always find more things to spend your money on if you do not make it a priority to save or reduce your debt. Do not continue until you have written down a percentage and dollar amount next to the words Savings and Debt Reduction.

For this to work, I have to have the money automatically withdraw from my account every time I get paid. I suggest you set that up, open a savings account if you don’t have one, and do not treat this account as a second checking account. Forget the money exists.

Step 4: The Super Simple Budgeting Technique

You may have not realized this, but if you followed all the steps, you have now created your own custom plan for saving and debt reduction and we haven’t even finished thinking about all your other expenses. That’s because financial stability is a commitment. It’s not based on how much is left over after the month. You’ll never accumulate wealth unless you are consciously making decisions on where and how you spend your money.

You should have three main buckets and the percentage of how much of your money goes to each – % fixed expenses, % savings/debt reduction, and % variable expenses.

Now that you know how much you have to work with on variable expenses, this is where budgeting comes in. You really only need to manage this budget on a daily basis.

For variable expenses, we are simply going to create two buckets – yay! I hate budgeting and I hate feeling like I have to track everything and categorize and recalculate budgets after every transaction every day.

The method I’m going to share came from Jordan Page at Fun, Cheap, or Free Free. Check out her video! To help you save time, start watching at 7:00 minutes. This is one of the things you don’t need to do right now, so let me briefly describe her concept.

You will have two buckets – groceries and other.

Let’s prioritize groceries since we need to eat. Her budgeting formula for groceries is to spend only $100 per person per month starting at $300. My household only has two people – myself and my husband. My grocery budget is $250, but I’ll ask my husband to grab eggs or milk when we’re running low, so for us $300 is about right. This may seem too low or too high for people, but if it’s too low, please remember that this is a budget for helping you become more financially stable. You will have to make sacrifices, say no, and think about how you can do more with less. If your pantry is filled with individually wrapped snacks and you have sodas or juice at home – you’re splurging! This could be separate blog post, so I will just say, use her formula as a baseline, shop the sales, and one key thing – only grocery shop once a week max. If you’re going more than once a week, you will spend more than you intent to.

In her method, she goes further and breaks down the amount by week, so that you know your budget at every grocery trip. I go grocery shopping once every 10 days or so because I hate grocery shopping, so I’m okay with keeping the monthly budget, but if you have kids or a bigger family, I would follow her method and break it down weekly. For example $400 monthly grocery budget would be $100 per week.

If her formula is too much, by all means, use an amount or percentage that will work for you and write it down.

Now that you have an amount for Groceries within your variable expenses, the remaining amount could technically go into your “Other” budget, but I would only do this if you feel like it’s tight and it will require discipline for you to stay within this budget.

Before we get into that, let me clarify what goes into this “other” budget. This is dining out, shopping, Uber, Starbucks, clothing, entertainment, gifts, and honestly if you’re a beginner and you’re trying to play around with stocks or other investments, please put this as an expense. Just write it off and if it makes you money, awesome! But if you don’t, you’re not eating into your priorities. I put vehicle gas and maintenance in this budget because it varies so much for me with working from home, but it can also go in your fixed expenses if you are consistently spending the same amount every month.

For a long time I would ensure my fixed expenses were low and that I saved some money. Then, I would spend the rest on whatever. I thoroughly regret this. This is where the 50/30/20 budget fails. For me, 30% of my money going to “wants” was too much especially with student loans and other things that I could be doing or paying off with this money.

Writing down a number is not difficult. What will be difficult here is actually sticking to it, remembering it exists, and tracking your expenses! I know, this is the part I could not fathom doing. Jordan Page recommends

keeping track of expenses on an envelope. See image below.

I know what you’re thinking. You’re just going to do this on your phone, right? I’ve tried tracking my expenses on my phone, and it does not work for me. If I’m doing it manually like on a note, I forget that I’m tracking these items. Many budget apps are just tracking your expenses and give you historical information. This can help you determine where you’re spending your money, but it doesn’t keep it top of mind. The alerts that I’ve surpassed my coffee budget does not help me after the fact.

The envelope method has actually worked for me. Although I’m not keeping my receipts, the envelope is a bit more sturdy than just a sheet of paper, so it’s easier to maintain. What I do is keep this on my night stand where I can see it every day before I sleep and when I wake up. Yes, I miss a day or two sometimes, but when I see it, I just write down what I’ve spend money on. If you don’t do any online shopping, keeping it in your wallet is another way to keep it top of mind.

Please do this – this is the part you’re most in control of. This is what makes the difference, so try it as first step. I’m not asking you to categorize this or create a budget for each expense. This is simple – write down what you spend and stay under your monthly or weekly budget.

Step 5: Maximize Saving and Paying Off Debts

This blog is long enough. If you want me to continue with Step 5 (my biggest mistake, by the way!), let me know. I can also answer questions about charity/tithing/donations and vacation money!

Let me know if there’s anything else I should include.

I hope this helps someone get started! It’s not easy and there’s way too much information out there. You really can’t go wrong starting here.

Leave a Reply